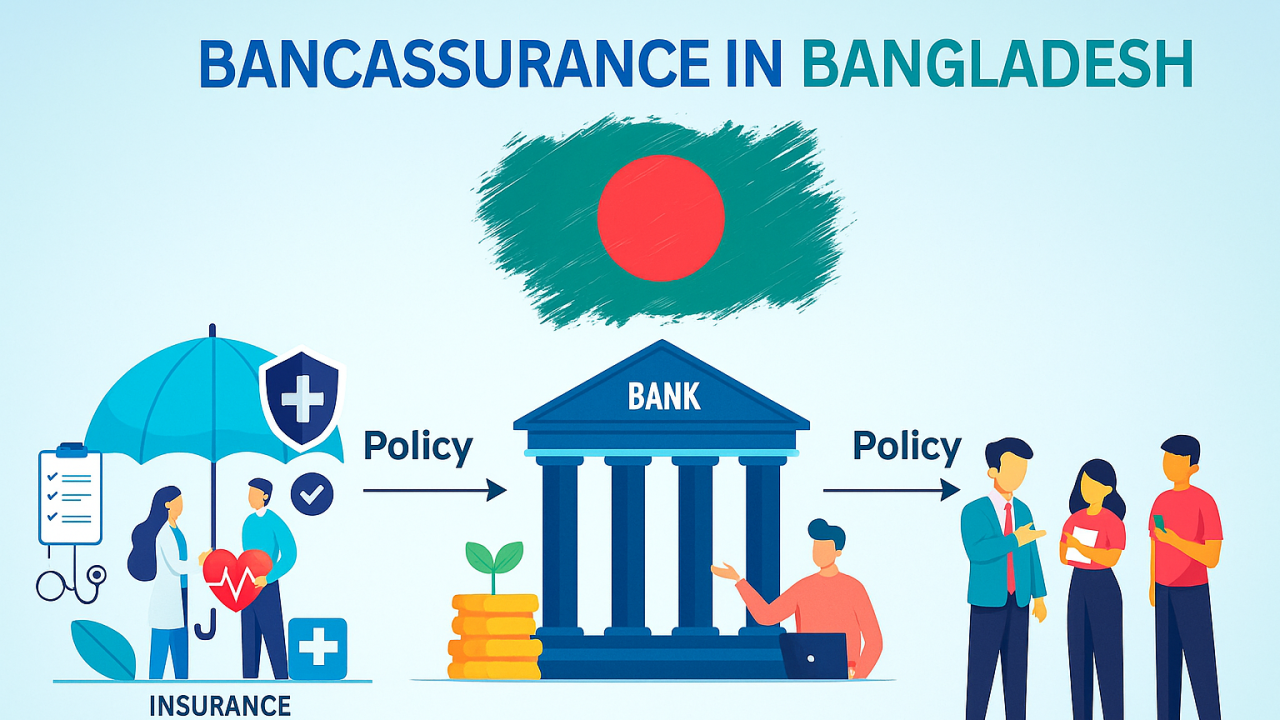

Bancassurance Under the Lens: India’s ambition to achieve “Insurance for All by 2047” has brought the bancassurance model into sharp focus. Bancassurance, where banks sell insurance products through their branches and distribution networks, has become one of the most powerful channels for expanding insurance coverage in the country. However, alongside its growth, concerns about mis-selling of insurance policies have emerged as a serious challenge. Industry experts believe that while bancassurance can play a major role in achieving universal insurance coverage, stronger regulations, better transparency, and improved consumer awareness are essential to ensure that customers receive suitable products.

The concept of Insurance for All by 2047, aligned with India’s long-term financial inclusion goals, aims to ensure that every citizen has access to adequate insurance protection. Banks, with their vast customer base and nationwide presence, are expected to be key partners in achieving this objective. At the same time, regulators and policymakers are working to address the issue of mis-selling to protect policyholders and strengthen trust in the insurance ecosystem.

Highlights of Bancassurance and Insurance for All by 2047

| Particulars | Details |

|---|---|

| Concept | Bancassurance |

| Goal | Insurance for All by 2047 |

| Main Concern | Mis-selling of insurance policies |

| Key Participants | Banks, insurance companies, regulators |

| Opportunity | Expanding insurance penetration |

| Challenge | Ensuring transparency and customer protection |

| Regulatory Focus | Strengthening consumer safeguards |

Understanding the Bancassurance Model

Bancassurance refers to the partnership between banks and insurance companies where banks distribute insurance products to their customers. This model allows insurers to leverage the extensive branch networks and customer relationships of banks.

For banks, bancassurance provides an additional source of revenue through commissions and distribution fees. For insurance companies, it offers access to a large customer base without building an extensive distribution network from scratch.

In India, bancassurance has grown rapidly because banks already have strong customer trust and widespread reach, particularly in semi-urban and rural areas. This makes it an effective channel for promoting life insurance, health insurance, and general insurance products.

The Vision of Insurance for All by 2047

The idea of Insurance for All by 2047 is part of India’s broader strategy to improve financial security and economic resilience. By ensuring that individuals and businesses have adequate insurance coverage, the country aims to reduce financial vulnerability caused by health emergencies, accidents, natural disasters, and other risks.

Currently, India’s insurance penetration remains relatively low compared to many developed economies. Expanding coverage requires reaching millions of underserved individuals who may not yet understand the importance of insurance.

Banks are expected to play a crucial role in this process because of their extensive distribution networks and existing relationships with customers.

The Issue of Mis-Selling in Bancassurance

While bancassurance offers significant growth opportunities, it has also raised concerns about mis-selling of insurance policies. Mis-selling occurs when customers are sold insurance products that are unsuitable for their financial needs or when policy details are not clearly explained.

In some cases, customers may purchase insurance products without fully understanding policy terms, premium commitments, or long-term benefits. This can lead to dissatisfaction and loss of trust in both banks and insurance companies.

Mis-selling may happen due to sales pressure on bank employees, lack of adequate product knowledge, or insufficient disclosure of policy details to customers.

Impact on Consumer Trust

Consumer trust is critical for the long-term growth of the insurance sector. When customers feel that they have been misled or sold inappropriate products, it can damage the reputation of both banks and insurance providers.

Mis-selling incidents can also discourage people from purchasing insurance in the future, which directly conflicts with the goal of expanding insurance coverage across the country.

Ensuring transparency and customer education is therefore essential for maintaining confidence in the bancassurance channel.

Regulatory Measures to Address Mis-Selling

Regulators have recognized the need to address mis-selling issues in the bancassurance sector. Authorities have introduced various guidelines to ensure that customers receive clear and accurate information about insurance products.

These measures focus on improving product disclosures, training for bank staff, and monitoring of sales practices. Regulators are also encouraging insurers and banks to adopt technology-driven systems that enhance transparency and reduce the chances of misleading sales practices.

In addition, customer grievance mechanisms are being strengthened to ensure that policyholders can easily report and resolve issues related to insurance sales.

Read about: RITES Recruitment 2026: Apply for 2 General Manager Posts in a Leading Government Engineering Consultancy

The Role of Technology and Digital Platforms

Technology can play a major role in reducing mis-selling and improving customer experience in the insurance sector.

Digital platforms can provide transparent product comparisons, detailed policy information, and simplified purchasing processes. When customers have access to clear and accurate information, they are better able to make informed decisions.

Banks and insurance companies are increasingly investing in digital insurance platforms, artificial intelligence tools, and data analytics to improve customer service and personalize insurance recommendations.

These technological innovations can help align insurance products with the specific needs of customers.

Balancing Growth and Consumer Protection

The future success of the bancassurance model depends on achieving the right balance between expanding insurance access and protecting consumer interests.

Banks have a unique opportunity to promote insurance awareness and financial planning among their customers. By providing proper guidance and recommending suitable products, they can help individuals secure their financial future.

At the same time, strong regulatory oversight and ethical sales practices are necessary to ensure that the bancassurance channel remains trustworthy and sustainable.

Future Outlook for India’s Insurance Sector

India’s insurance sector is expected to grow significantly in the coming decades as economic development, rising incomes, and financial awareness increase demand for insurance products.

The bancassurance model will likely remain a key distribution channel because of its ability to reach large numbers of customers efficiently.

However, achieving the vision of Insurance for All by 2047 will require collaboration between regulators, banks, insurance companies, and technology providers. By addressing mis-selling concerns and focusing on customer-centric solutions, the industry can build a stronger and more inclusive insurance ecosystem.

FAQs About Bancassurance Under the Lens

What is bancassurance in the insurance sector?

Bancassurance is a partnership where banks distribute insurance products to their customers on behalf of insurance companies.

Why is mis-selling a concern in bancassurance?

Mis-selling occurs when customers are sold unsuitable insurance products or are not given complete information about policy terms, which can lead to dissatisfaction and loss of trust in the insurance industry.