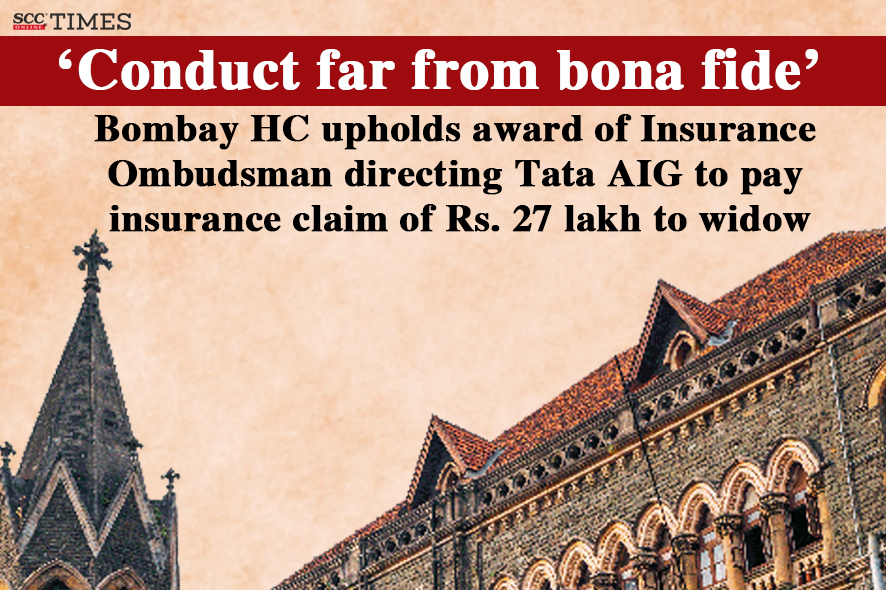

Denial of Housing Loan Insurance Claim: In a landmark decision, the Bombay High Court has directed Tata AIG General Insurance to pay Rs 27 lakh along with interest to a widow within four weeks, after the company initially rejected her housing loan insurance claim. This verdict underscores the judiciary’s firm stance on protecting policyholders’ rights, especially when insurers attempt to deny legitimate claims.

The case revolves around a housing loan insurance policy that was linked to a loan sanctioned by India Infoline Housing Finance Ltd (IIFL). The insurance policy was intended to secure repayment of the loan in the event of the borrower’s death or incapacitation. Unfortunately, in April 2021, the widow’s husband suffered a sudden cardiac arrest in the hospital and died within 15 to 20 minutes. Tata AIG initially rejected the claim, citing insufficient medical documents proving that the death was due to a critical illness covered by the policy.

Background of the Case: How the Dispute Began

In June 2017, IIFL approved a housing loan of Rs 27 lakh to the woman’s husband, mandating an insurance policy as part of the agreement. On April 15, 2021, he experienced a severe cardiac arrest and passed away in the hospital within a short time. Despite the clear objective of the insurance policy to cover such unfortunate events, Tata AIG rejected the claim in October 2021. The insurer argued that there was no substantial medical documentation to support that the death was caused by a critical illness included in the policy.

Subsequently, in November 2021, the widow provided a letter from her husband’s treating doctor, affirming that he had suffered a heart attack. The insurance ombudsman reviewed the case and, in November 2022, directed Tata AIG to pay the full claim amount of Rs 27 lakh.

Dispute Over Cause of Death

Tata AIG’s defense hinged on a report by their panel doctor, who reviewed the case papers and concluded that the treatment was for an infection and Covid-19, not a heart attack. This created a conflict of medical opinions, further complicating the claim process.

However, Justice Sandeep Marne rejected Tata AIG’s appeal on September 3, 2025. He emphasized that the treating doctor’s statement – indicating that death occurred minutes after the onset of chest pain – carried more weight than the insurer’s paper-based review. The judge noted that breathlessness and chest pain were classic symptoms of a heart attack, and even if the insured was treated for Covid-19 and sepsis, this did not preclude a cardiac arrest.

Justice Marne stated, “The panel doctor’s report, based only on paper review, cannot be blindly accepted.” He pointed out that the purpose of the insurance policy was to safeguard against such unfortunate events, and Tata AIG’s attempt to wriggle out of its obligation was unjustified.

Read about: Insurance Ombudsman Directs National Insurance to Pay for Dental Surgery Claim

The Courts Verdict and Its Implications

The court upheld the insurance ombudsman’s order, reinforcing that the widow’s claim was legitimate and valid. In addition to the Rs 27 lakh payout, interest at the applicable bank rate plus 2% from the date of claim rejection was also awarded. Although the judge refrained from imposing additional costs on Tata AIG, he strongly criticized the insurer’s prolonged litigation strategy, which forced the widow to battle for four years to obtain rightful compensation.

This ruling sets a significant precedent in India’s insurance sector, emphasizing that insurers must act in good faith and that disputes should not be unnecessarily dragged out at the expense of policyholders.

Conclusion

The Bombay High Court’s ruling against Tata AIG marks a pivotal moment in protecting consumer rights within the insurance industry. It highlights the crucial role of treating doctors’ firsthand opinions over panel doctors’ desk reviews when it comes to validating insurance claims. The court’s decision stresses the principle that the primary objective of insurance is to provide financial security to policyholders in their time of need, not to complicate or deny rightful claims.

For policyholders across India, this verdict serves as a powerful reminder to remain vigilant and proactive when dealing with insurance companies. It also encourages prompt filing of claims and persistence in pursuing justice if claims are unfairly denied.

As the insurance sector continues to face scrutiny over its claim settlement practices, this ruling could catalyze more consumer-friendly reforms and encourage insurers to act more responsibly.

FAQs Denial of Housing Loan Insurance Claim

Q1: Why did Tata AIG initially reject the housing loan insurance claim?

A1: Tata AIG rejected the claim in October 2021, stating that there was insufficient medical documentation proving that the death was due to a critical illness covered by the policy. The insurer argued that the deceased had been treated for Covid-19 and sepsis infection, not a heart attack.

Q2: What was the role of the insurance ombudsman in this case?

A2: The insurance ombudsman reviewed the submitted evidence, including a letter from the treating doctor confirming a heart attack as the cause of death. In November 2022, the ombudsman directed Tata AIG to pay the full Rs 27 lakh, recognizing the widow’s claim as valid and justified.

Q3: How did the court view the panel doctor’s report compared to the treating doctor’s opinion?

A3: The Bombay High Court held that the panel doctor’s report, based solely on a paper review, could not be blindly accepted. Instead, the opinion of the treating doctor who directly treated the insured held greater credibility, especially since the death occurred within minutes of chest pain, not allowing time for extensive diagnostics.

Q4: What was the final order of the Bombay High Court?

A4: The Bombay High Court dismissed Tata AIG’s appeal and ordered the company to pay Rs 27 lakh plus applicable interest within four weeks. The interest was calculated at the applicable bank rate plus 2% from the date of claim rejection until payment.

Q5: What does this ruling mean for policyholders in India?

A5: This ruling reinforces the principle that insurance companies must honor legitimate claims in a timely and fair manner. It emphasizes the importance of the treating doctor’s firsthand medical opinion in settling disputes over cause of death. The decision also discourages insurers from unnecessarily delaying or denying rightful claims, potentially influencing more consumer-friendly practices in India’s insurance industry.