Insurance Mis-Selling in India: As the financial year-end approaches, many Indians notice a familiar pattern: a sudden spike in calls from unknown numbers, friendly voices that already seem to know personal details like your age, bank account, salary range, or even future plans. These callers promise tax savings, guaranteed returns, or limited-period benefits. The pitch sounds professional, urgent, and trustworthy—often enough to convince even financially aware individuals. This is the reality of insurance mis-selling in India, a problem that has grown steadily over the years.

What Is Insurance Mis-Selling?

Insurance mis-selling occurs when a policy is sold by providing incomplete, misleading, or false information, or when a product is sold to a customer for whom it is clearly unsuitable. This includes selling high-premium policies to people who need basic protection, exaggerating returns, hiding lock-in periods, or presenting insurance as a “fixed deposit” or “tax-saving investment” without explaining the risks and costs.

In many cases, customers realise the mistake only months or even years later—often when they attempt to exit the policy and face heavy penalties.

Why Financial Year-End Is Peak Season for Mis-Selling

March is notorious for aggressive insurance sales. Banks, agents, and relationship managers face strict annual targets, and insurance products offer higher commissions than many other financial instruments. This pressure leads to rushed sales, half-truths, and emotional persuasion tactics.

Read about: Planette Launches Joro

The Role of Banks in Mis-Selling

One of the most concerning aspects is the role played by banks, which enjoy a high level of trust among customers. Bank relationship managers often cross-sell insurance products, leveraging existing customer data and long-standing relationships.

Many customers assume the product is being recommended in their best interest, not realising that:

- Bank staff earn incentives for selling insurance

- The product may not align with the customer’s financial goals

- Cheaper or more suitable alternatives may exist outside the bank

Commonly Mis-Sold Insurance Products

Some insurance products are more prone to mis-selling than others:

- ULIPs (Unit Linked Insurance Plans): Marketed as high-return investments while downplaying market risks and charges.

- Endowment Plans: Sold as wealth-creation tools despite offering low long-term returns.

- Single-premium policies: Pitched to senior citizens without explaining liquidity constraints.

- Child or pension plans: Often unsuitable but sold emotionally.

Why Customers Fall for It

Insurance contracts are complex, filled with technical jargon and fine print. Combined with time pressure and trust in the seller, many buyers:

- Do not fully understand exclusions and lock-in periods

- Confuse insurance with investment products

- Assume verbal assurances are legally binding

Regulatory Challenges and Gaps

Regulators like IRDAI have issued guidelines against mis-selling and introduced measures such as free-look periods and standard disclosures. However, enforcement remains difficult due to:

- Large distribution networks

- Verbal sales pitches that are hard to prove later

- Limited awareness among customers about complaint mechanisms

Many victims do not know they can approach the insurer, IRDAI, banking ombudsman, or consumer courts.

Also read: Ignoring the HPV Vaccine? The Myths Putting Indian Girls at Risk

How Consumers Can Protect Themselves

Awareness is the first line of defence. Customers should:

- Never buy insurance solely for tax savings

- Ask for written benefit illustrations

- Compare products independently

- Use the free-look period to cancel unsuitable policies

- Remember: insurance is for protection, not guaranteed returns

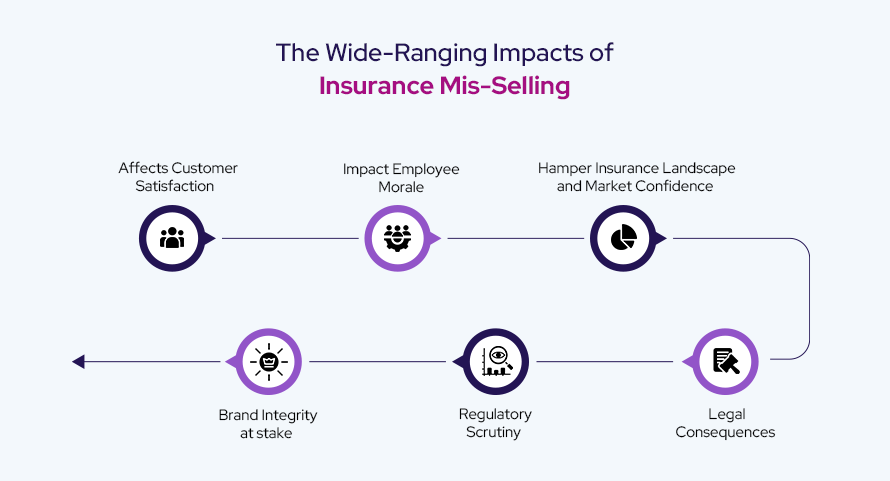

Conclusion

Insurance mis-selling in India is not just a sales issue—it is a trust issue. As banks and agents chase targets, customers often pay the price through unsuitable policies and long-term losses. Stronger regulation, better enforcement, and higher financial literacy are essential to curb this practice. Until then, consumers must remain cautious, ask uncomfortable questions, and remember that urgency in finance is often a red flag, not an opportunity.

Frequently Asked Questions

1. What is the most common form of insurance mis-selling in India?

Selling investment-linked insurance plans as guaranteed or risk-free products is one of the most common forms.

2. Can I cancel a mis-sold insurance policy?

Yes, most policies offer a free-look period (usually 15–30 days) during which you can cancel without major penalties.

3. Are banks allowed to sell insurance products?

Yes, but they must disclose all terms clearly and ensure the product is suitable for the customer.

4. Where can I complain about insurance mis-selling?

You can complain to the insurer, IRDAI, the banking ombudsman, or approach consumer courts if required.